Regime Analytics Features

Everything you need to read the market

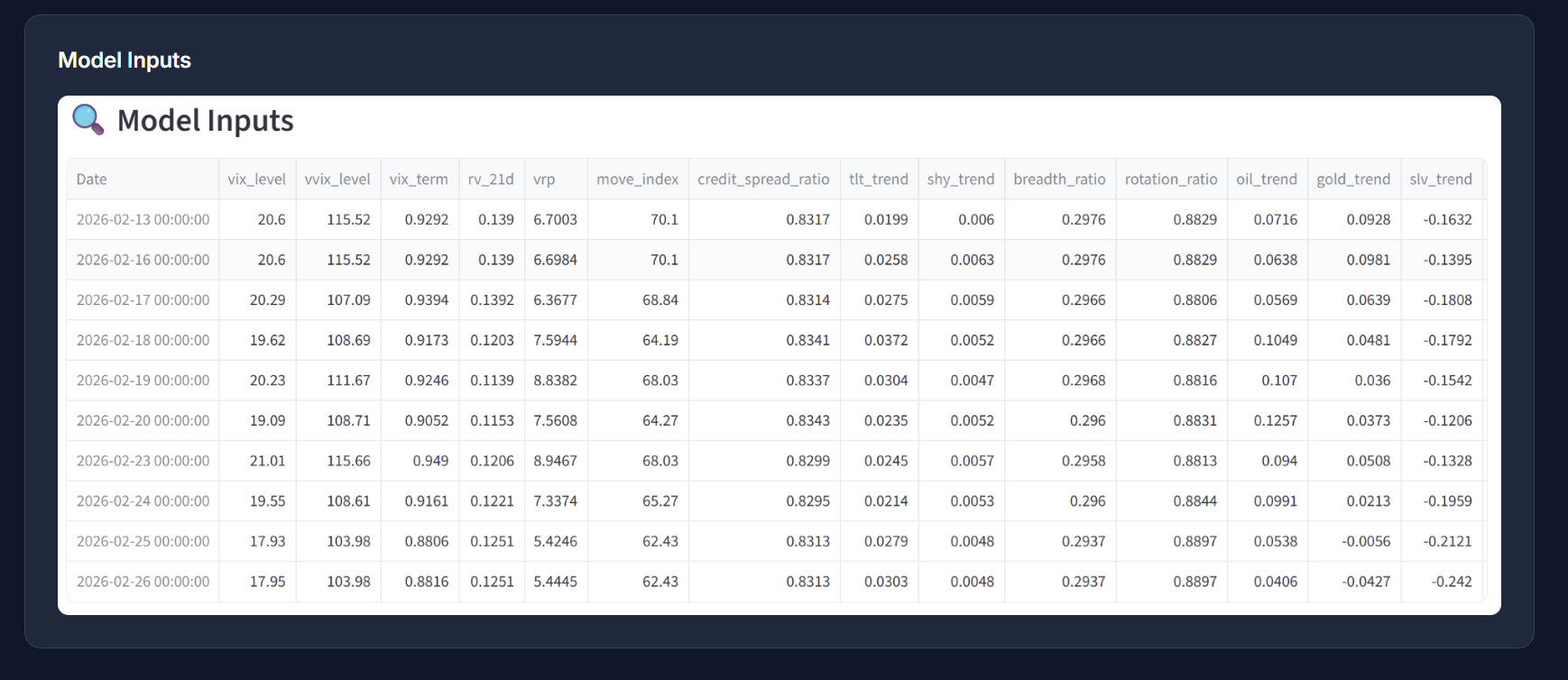

Our HMM-based system processes comprehensive market data to give you a clear, probabilistic view of current and future market conditions.

Real-Time Regime Detection

4-state HMM identifies Bull, Neutral, Bear, and High Volatility regimes using comprehensive market data with probability-weighted confidence scores.

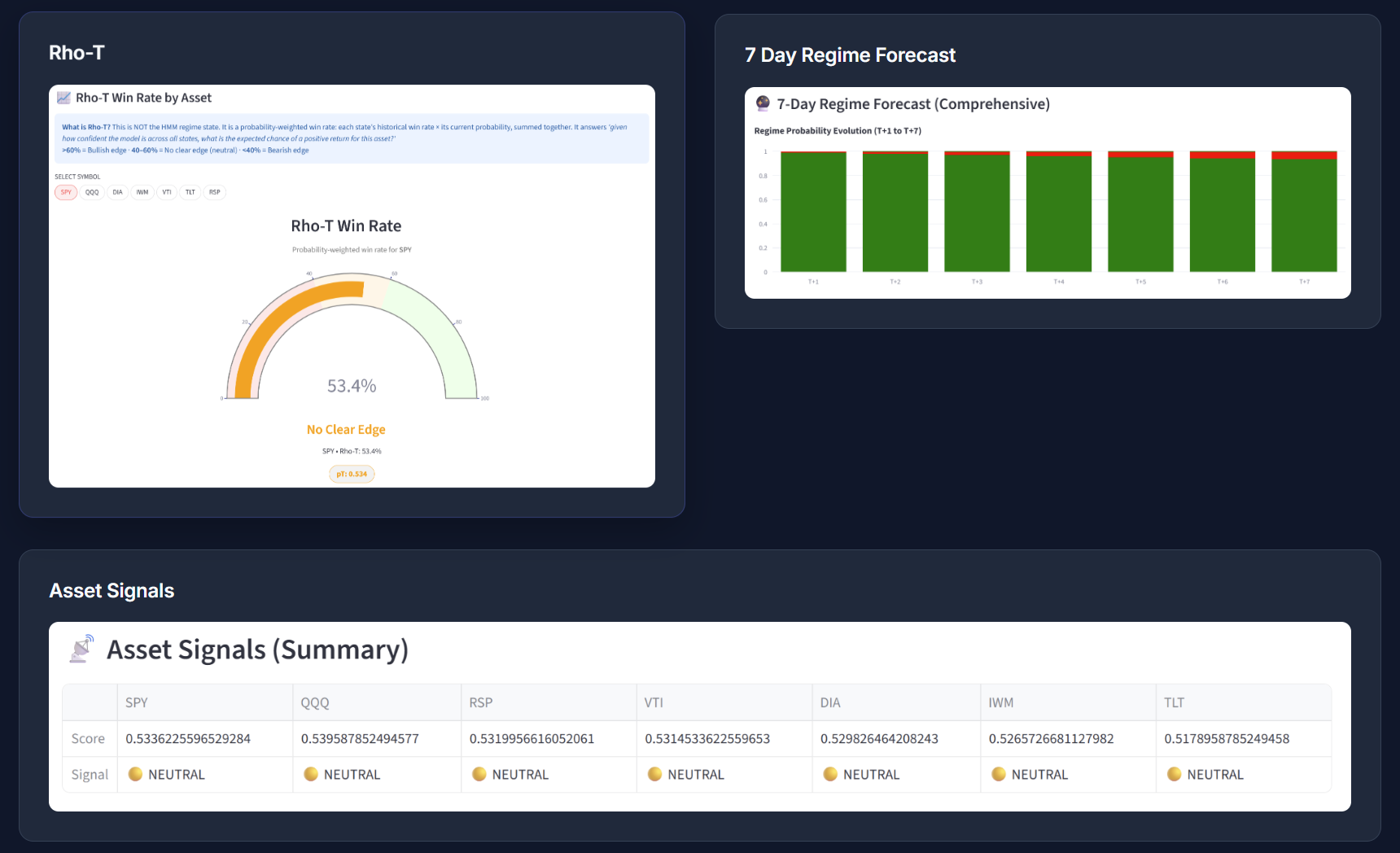

Multi-Asset Signals

Probability-weighted win rates (Rho-T) across SPY, QQQ, DIA, IWM, VTI, TLT, and RSP. See how each asset performs in every regime.

7-Day Forecast

Forward-looking regime probability evolution using transition matrix projections. See where the market is likely headed before it moves.

15-Year History

Full historical regime analysis going back to 2010. Understand how markets have shifted through every major event and crisis.

Volatility Metrics

Advanced volatility surface analysis including regime-conditional vol metrics and cross-asset correlation breakdowns.

Research-Backed

Built on validated Hidden Markov Model methodology with walk-forward testing and stress-tested against out-of-sample data.

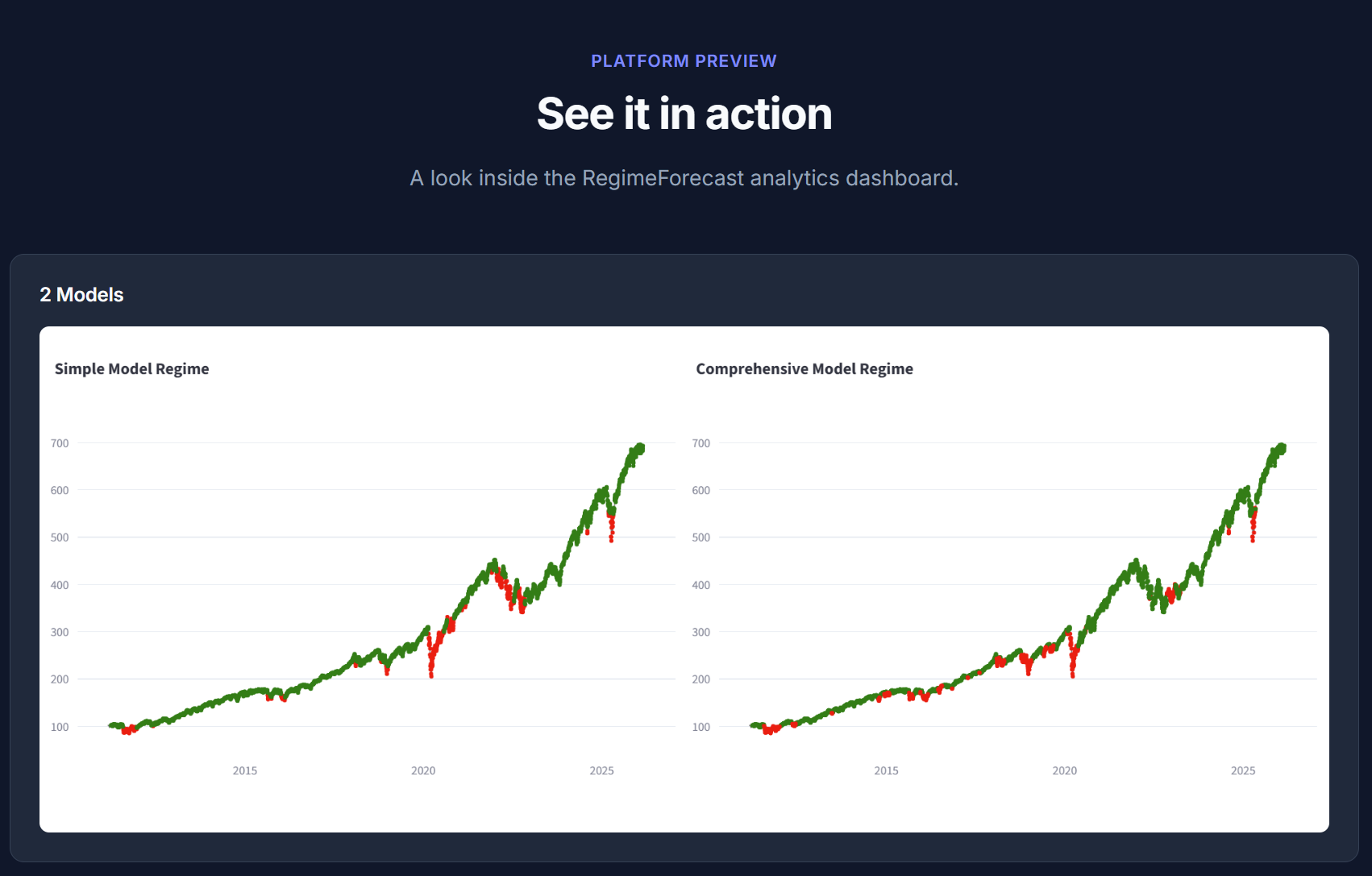

Platform Preview

See it in action

A look inside the RegimeForecast analytics dashboard.

Behind the Math

Probabilistic regime inference, not guesswork

RegimeForecast is built on ensemble Hidden Markov modeling techniques. The objective is to estimate latent market states from observable return behavior and volatility structure.

What is Rho-T?

Each response from the RegimeForecast system includes a value called rhoT (rho at time t) — the current model-implied probability that market conditions resemble historically favorable environments.

Rather than labeling markets as simply "bullish" or "bearish," rhoT quantifies regime alignment on a continuous scale. Higher values indicate stronger similarity to historical periods associated with constructive return environments.

Hidden Markov Regime Modeling

Hidden Markov Models assume that observed financial returns are generated by an underlying, unobserved state process that transitions between discrete regimes over time.

These latent states may correspond to:

- Persistent trend phases

- Transitional markets

- Volatility clustering regimes

- Risk-off conditions

Ensemble Architecture

Rather than relying on a single HMM configuration, RegimeForecast employs a diversified ensemble of models trained with varying assumptions and statistical structures.

- Gaussian HMMs with varying state counts

- Mixture-distribution HMMs for non-normal return behavior

- Variational Bayesian HMMs for regularized estimation

This diversification reduces model-specific bias and improves robustness across market environments.

Adaptive Model Selection

To avoid overfitting and improve adaptability, the framework incorporates a dynamic model selection process.

At each evaluation point, a portion of predictions are selected from historically strong-performing models, while a smaller proportion are drawn from alternative models to maintain diversity.

The goal is not model perfection, but durable signal behavior across market cycles.

Signal Processing & Stabilization

Raw model outputs undergo post-processing to enhance stability and usability:

- Confidence Filtering — Prevents excessive regime oscillation during noisy periods

- Temporal Smoothing — Reduces variance in daily regime probabilities

- Probability Normalization — Ensures rhoT remains interpretable as a regime-alignment measure

Designed For

RegimeForecast provides probabilistic context — not directional trade signals.

See It In Action

Watch the Platform Walkthrough

A quick tour of the dashboard — regime signals, 7-day forecast, asset signals, and the Rho-T indicator.

Ready to see your regime edge?

Start your 14-day free trial and get full access to all features.

Start 14-Day Free TrialNo charge until day 15. Cancel anytime.